7 Investment sins

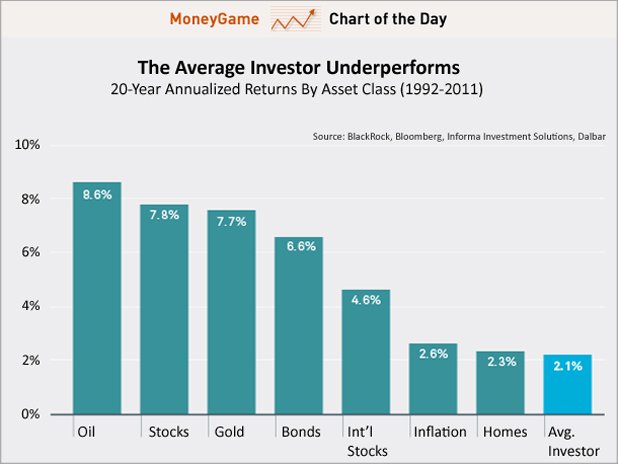

Hate to burst your bubble, but you are probably not a great investor. Need proof? Check out this chart from Blackrock that shows just how poorly average investors have been doing over the past two decades:

From 1992 – 2011, the average investor has only seen a 2.1 annualized return, compared to 7.8 percent for stocks and 6.6 percent for bonds. The explanation is obvious: investors feel good as asset levels rise, prompting them to buy; then after the asset plunges, some of those same investors panic and cash out.

The problem becomes even more pronounced during times of extreme market volatility and can leave a lasting impression. According to Bankrate.com’s Financial Security Index, a whopping 76 percent of respondents are simply avoiding stocks. Evidently, the combination of the worst recession since the Great Depression, plus the 55 percent stock market wipeout from October 2007 to March 2009 has made investors gun shy.

Economists call this “recency bias,” which means that we use our recent experience as a guide for what will happen in the future. So when stocks are soaring, we think markets will keep rising, but when the market plunges, we become convinced that it will never go up again.

Recency bias is just one of the 7 investment sins that continue to trip up investors—here are six more:

Allowing your emotions to rule your financial choices. There are two emotions that tend to overly influence our financial lives: fear and greed. At market tops, greed kicks in and we tend to assume too much risk. Conversely, when the bottom falls out, fear takes over and makes us want to sell everything and hide under the bed.

Not maintaining a diversified portfolio. One of the best ways to prevent the emotional swings that every investor faces is to create and adhere to a diversified portfolio that spreads out your risk across different asset classes, such as stocks, bonds, cash and commodities. (Owning 5 different stock funds does not qualify as a diversified portfolio!)

Timing the market. Repeat after me: “Nobody can time the market. Nobody can time the market.” One of the big challenges of market timing is that requires you to make not one, but two lucky decisions: when to sell and when to buy back in.

Paying more fees than necessary. Why do investors consistently put themselves at a disadvantage by purchasing investments that carry hefty fees? Those who stick to no-commission index mutual funds start each year with a 1-2 percent advantage over those who invest in actively managed funds that carry a sales charge.

Assuming too big a risk. If you are going to make a risky investment, such as purchasing a large position in a single stock or making an investment in a tiny company, only allocate the amount of money you are willing to lose, that is, an amount that will not really affect your financial life over the long term. Yes, there are people who invest in the next Google, but just in case things don't work out, limit your exposure to a reasonable percentage (single digits!) of your net worth.

Not asking for help. There are plenty of people who can manage their own financial lives, but there are also many cases where hiring a pro makes sense. Make sure that you know what services you are paying for and how your advisor is compensated. It’s best to hire a fee-only or fee-based advisor who adheres to the fiduciary standard, meaning he is required to act in your best interest. To find a fee-only advisor near you, go to NAPFA.org.